Main Takeaways

- Demand for softwood lumber and structural panels is expected to remain under pressure as single-family housing starts face challenges, including elevated mortgage rates, high house prices, and rising construction costs.

- In southern Georgia counties impacted by Hurricane Helene, pulpwood prices are expected to stay low through most of 2025 as mills continue to process salvaged timber.

- Affected areas may experience rising pine sawtimber prices in 2025 because of an inventory shortage.

Timber Prices in 2024

The southwide average stumpage prices for major timber products showed mixed trends in 2024. Pine sawtimber prices fell over $2 (9%) in Q3 to their lowest level since Q3 2020, after stabilizing near $26/ton for 2 years (TimberMart-South, 2024). Pine chip-n-saw prices declined slightly, down $0.60 (3%) to $17–18/ton from their stable levels since Q2 2022. However, hardwood sawtimber prices reached a recent high of $35/ton in Q3. Meanwhile, pine and hardwood pulpwood prices halted their declining trend since 2022, stabilizing at $7–8/ton. That is more than 30% below their early 2022 peak and 15% below prepandemic levels.

Timber markets in the U.S. South are primarily local because of the bulky nature of logs, which limits their transport to mills within a 50–75 mile radius (Conrad et al., 2017). Therefore, timber prices vary greatly by state and subregion. In Q3 2024, pine sawtimber prices fell across most southern timber regions, with significant drops of 20% in areas like South Georgia, Florida, and South Louisiana, and smaller declines of 5%–8% in Alabama and South Carolina. North Georgia and Tennessee were exceptions, with stable or rising prices.

In South Georgia, pine sawtimber and pine chip-n-saw prices dropped significantly after three consecutive quarters of growth in Q3. Pine sawtimber prices averaged $26.60/ton, down 20% from Q2 and 11% year over year. Pine chip-n-saw prices dropped to about $20/ton, a 10% decrease year over year. Mixed hardwood sawtimber averaged over $31/ton, down 9% from Q2 but still 8% higher than a year ago. Pine pulpwood prices were slightly above $15.50/ton. Hardwood pulpwood held steady at around $8/ton.

In North Georgia, pine sawtimber prices rose to $24–25/ton in Q3, up 20% year over year. This is the highest that prices have been since Q1 2023. Pine chip-n-saw averaged over $18/ton, up 7% from Q2 and 25% year over year. Mixed hardwood sawtimber prices of the region averaged over $35/ton, up 21% year over year. Pine and hardwood pulpwood prices stayed around $8/ton.

Like many other southern timber regions, the sharp decline in South Georgia’s pine sawtimber prices mainly was due to curtailment and downtime at several lumber mills. These include reduced hours at Canfor’s mills in Moultrie, GA, and Estill, SC; indefinite curtailments at Interfor’s mills in Meldrim, GA, and Summerville, SC; and temporary production cuts at six other Interfor mills in South Georgia.

Weakened market demand was the primary reason behind these cutbacks. Persistent inflation and high interest rates over recent years have eroded housing affordability and slowed the recovery in single-family housing starts, weakening the demand for softwood lumber products. Slower growth in remodeling and repairs also played a role. Lumber producers adjusted their output to align with demand and maintain profitability.

The impact of Hurricane Helene on Georgia’s timber market is not reflected in the Q3 prices. The hurricane made landfall on September 26, causing severe damage to Georgia’s forest sector. It caused significant timber losses, mill power outages, challenges in salvaging and processing damaged timber, and reforestation needs. Sawmills typically accept storm-damaged timber for 8–10 weeks until blue stain shows, while pulp and paper mills may process it for up to 8 months. As a result, sawtimber prices in the affected areas (mainly South Georgia) are expected to decline through late 2024. Pulpwood prices may remain low through mid-2025 due to an influx of salvaged timber. Additionally, the low efficiency of logging storm-damaged timber increases logging costs, leading to lower stumpage prices for timber owners.

2025 Outlook

Looking ahead, several factors will influence the timber markets in 2025.

Demand Factors

Key factors include housing markets, lumber mill capacity and production adjustment, pulp and paper mill closures and conversions, tariffs on Canadian lumber imports, immigration policies, and overall economic growth.

Over 70% of U.S. softwood lumber and structural panels are used in residential construction, particularly single-family homes, and home improvement activities (Alderman, 2022). While the Fed’s rate cuts in 2024 and two expected cuts in 2025 may ease construction costs, housing starts are likely to remain under pressure next year. Mortgage rates are expected to stay high because of inflation concerns, strong economic growth, tariffs, and slower rate cuts. Elevated mortgage rates, high home prices, and potential rising construction costs from a labor shortage will likely limit housing starts in 2025.

As of November 2024, single-family housing starts fell 10.2% year over year to a seasonally adjusted annual rate of 1.01 million units (U.S. Census Bureau, 2024). Single-family building permits, a leading indicator, declined 2.7% to 972,000 units. Projections for 2025 single-family housing starts range from 995,000 units (Fannie Mae, 2024), 1.11 million units (National Association of Realtors, 2024), to 1.13 million units (Mortgage Bankers Association, 2024)—all below the long-term trend of 1.2 million units. However, remodeling and repairing activities, after a slowdown in 2024, are expected to expand in 2025 (Joint Center for Housing Studies, 2024).

Tariffs on softwood lumber imports from Canada have nearly doubled since August 2024 and are expected to rise to 30% in 2025. While the increased tariffs may reduce Canadian imports and promote U.S. domestic production in the long run, they may drive up construction costs in the short run.

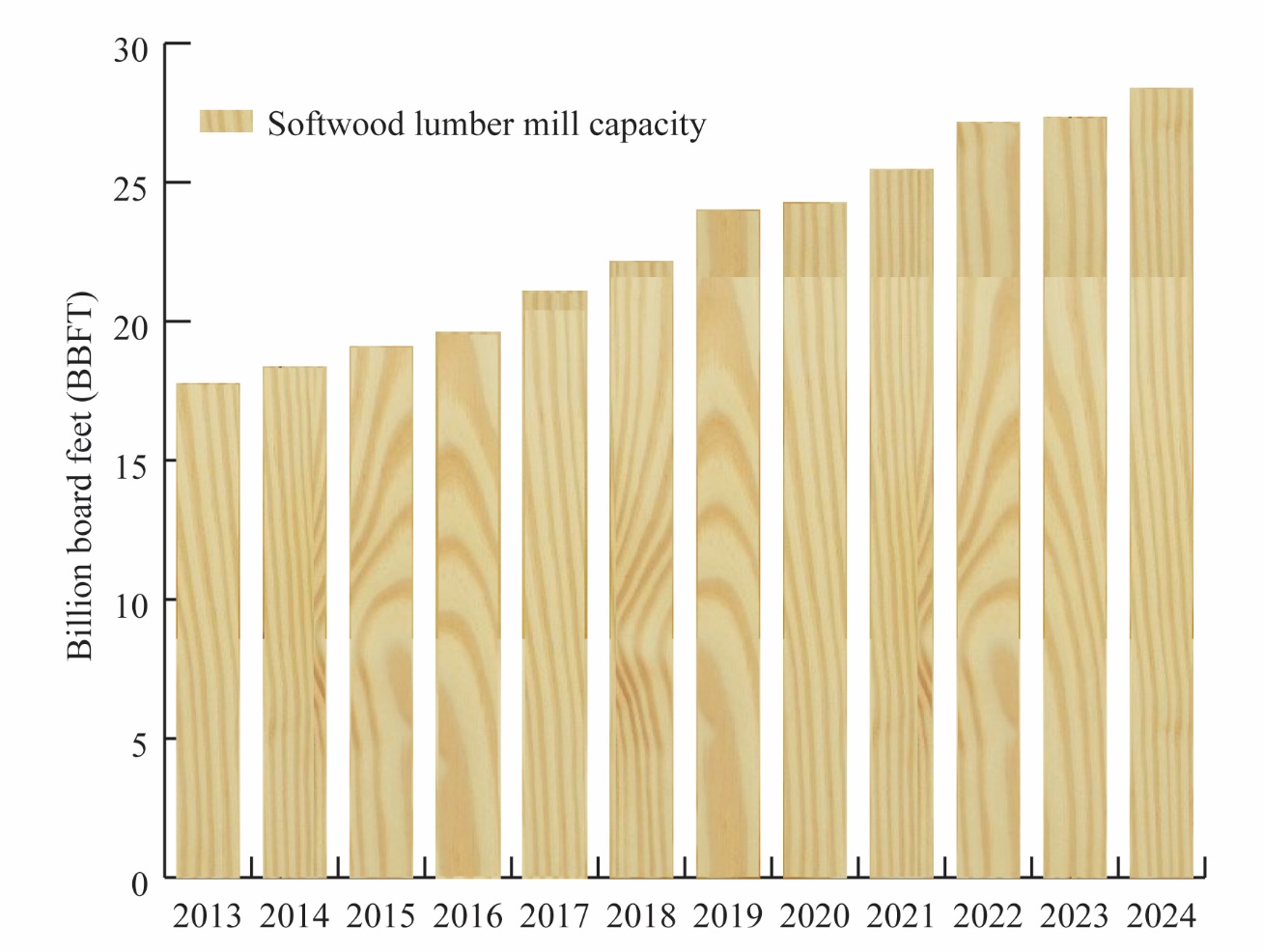

The U.S. South remains a preferred destination for softwood lumber and wood-using pulping investment because of abundant timber resources, a skilled workforce, and well-developed infrastructure. Southern softwood lumber mill capacity exceeded 28.4 billion board feet in 2024—a 35% increase from 2017 (Figure 1)—with an additional 753 million board feet by 2026 (Forisk, 2024). Canadian lumber companies account for much of this expansion because of reduced log availability in Western Canada and U.S. tariffs. However, southern softwood lumber mill utilization rates have declined from 85% in 2021 (Forisk, 2024) to 74% in 2024 because of weaker lumber demand.

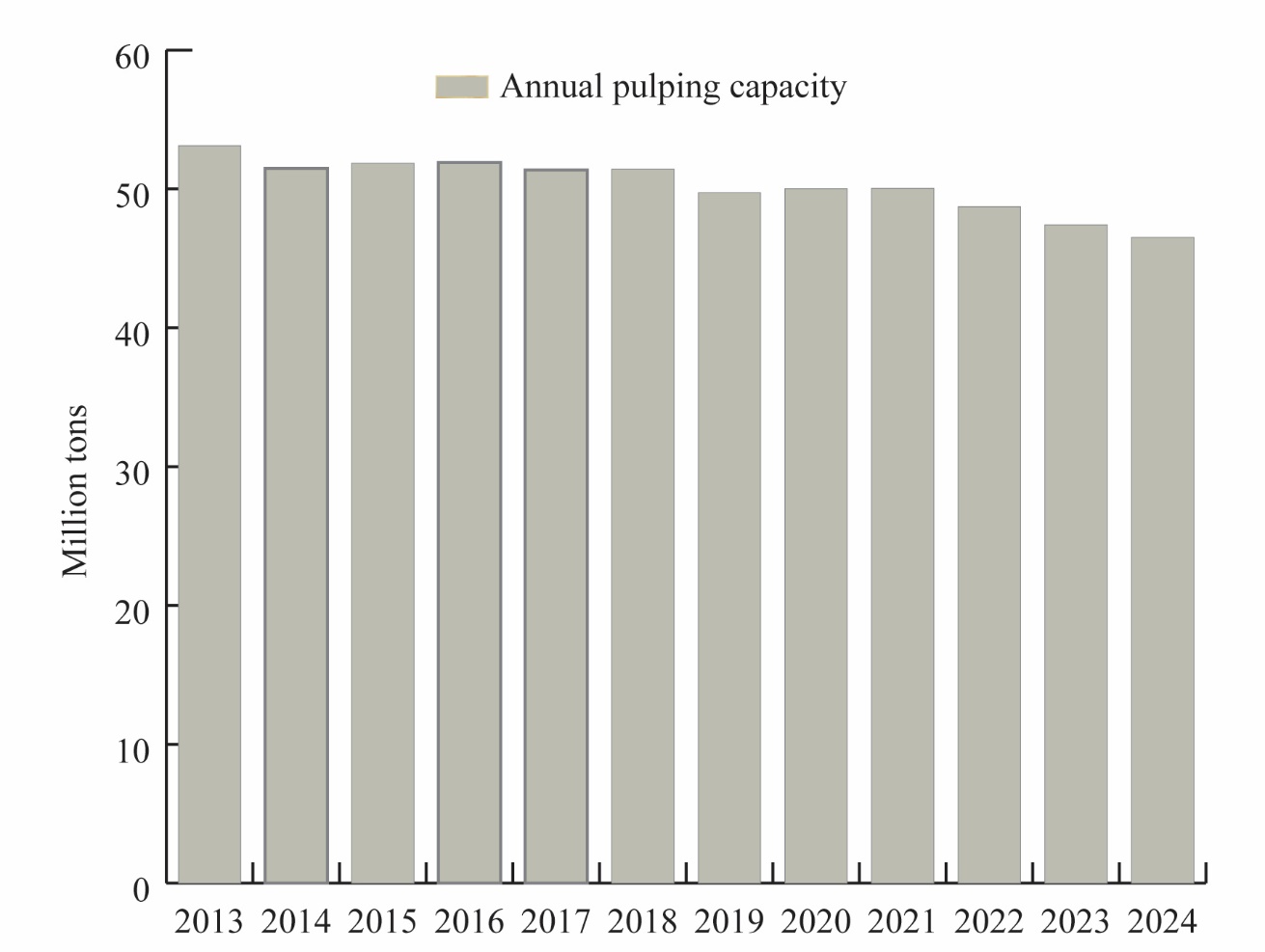

Meanwhile, southern wood-using pulping capacity continued to decline in 2024 because of product shifts in the paper and paperboard industries and increased utilization of recycled fiber for pulp production (Figure 2). This trend is expected to keep pulpwood prices down, particularly in regions affected by Hurricane Helene and areas with recent paper mill closures.

Supply Factors

Key supply-side factors include the salvage of hurricane-damaged timber, reduced timber inventory in affected areas, additional timber supply because of mill closures in adjacent areas, and logging capacity constraints.

In most southern timber regions, an oversupply of sawtimber from a decade of underbuilding will likely keep downward pressure on pine sawtimber prices. However, southern Georgia counties devastated by Hurricane Helene may experience tighter timber supply and rising sawtimber prices because of local inventory shortages, particularly in areas with low growth-to-drain ratios (U.S. Forest Service, 2024).

Hurricane Helene impacted 8.9 million acres of Georgia’s forestland, including some of the state’s most productive timberland (Georgia Forestry Commission, 2024). The damaged pine timber is equivalent to the state’s annual timber harvest. While pulpwood prices in the affected region may stay low through mid-2025 as mills absorb salvaged timber, sawtimber prices are expected to rise for several years as these areas recover.

References

Alderman, D. (2022). U.S. forest products annual marketing review and prospects, 2015–2021. U.S. Department of Agriculture Forest Service. https://research.fs.usda.gov/treesearch/64129

Conrad, J. L., IV, Demchik, M. C., & Vokoun, M. M. (2018). Effects of seasonal timber harvesting restrictions on procurement practices. Forest Products Journal, 68(1), 43–53. 10.13073/FPJ-D-16-00056

Fannie Mae. (2024). Housing forecast: December 2024. https://www.fanniemae.com/media/54381/display

Forisk. (2024). North American mill capacity database. https://forisk.com/product/north-american-forest-industry-capacity-database/

Georgia Forestry Commission. (2024). Hurricane Helene recovery assistance. https://gatrees.org/forest-management-conservation/natural-disaster-recovery/hurricane-helene-recovery-assistance/

Joint Center for Housing Studies. (2024). Leading indicator of remodeling activity (LIRA). Harvard University. https://www.jchs.harvard.edu/research-areas/remodeling/lira

Mortgage Bankers Association. (2024). MBA mortgage finance forecast. https://www.mba.org/news-and-research/forecasts-and-commentary

National Association of Realtors. (2024). Economic and housing market outlook as of October 2024. https://www.nar.realtor/sites/default/files/2024-10/forecast-q3-2024-us-economic-outlook-10-04-2024.pdf

TimberMart-South. (2024). Quarterly market news. https://timbermart-south.com/industry-reports/quarterly-market-news/

U.S. Census Bureau. (2025). Monthly new residential construction, December 2024. https://www.census.gov/construction/nrc/pdf/newresconst.pdf

U.S. Forest Service. (2024). EVALIDator and FIADB-API [Computer software]. U.S. Department of Agriculture. https://research.fs.usda.gov/products/dataandtools/tools/evalidator-and-fiadb-api

Status and Revision History

In Review on Jan 21, 2025

Published on Jan 22, 2025