Main Takeaways

- The Georgia dairy forecast for 2025 is steady to positive.

- Key uncertainties come from the balance of supply and demand and potential federal order reform.

- Highly pathogenic avian influenza (HPAI) and export risks may also play a role in the year ahead.

The upcoming year is forecast to be steady with an important theme of assessing where supply and demand will balance. Looking ahead, tailwinds for the sector include stable U.S. demand and a generally low feed-cost outlook. Headwinds arise from potential trade uncertainty and a risk that growing supplies drag down prices. HPAI remains a wildcard, and changes to federal milk marketing orders should be closely watched.

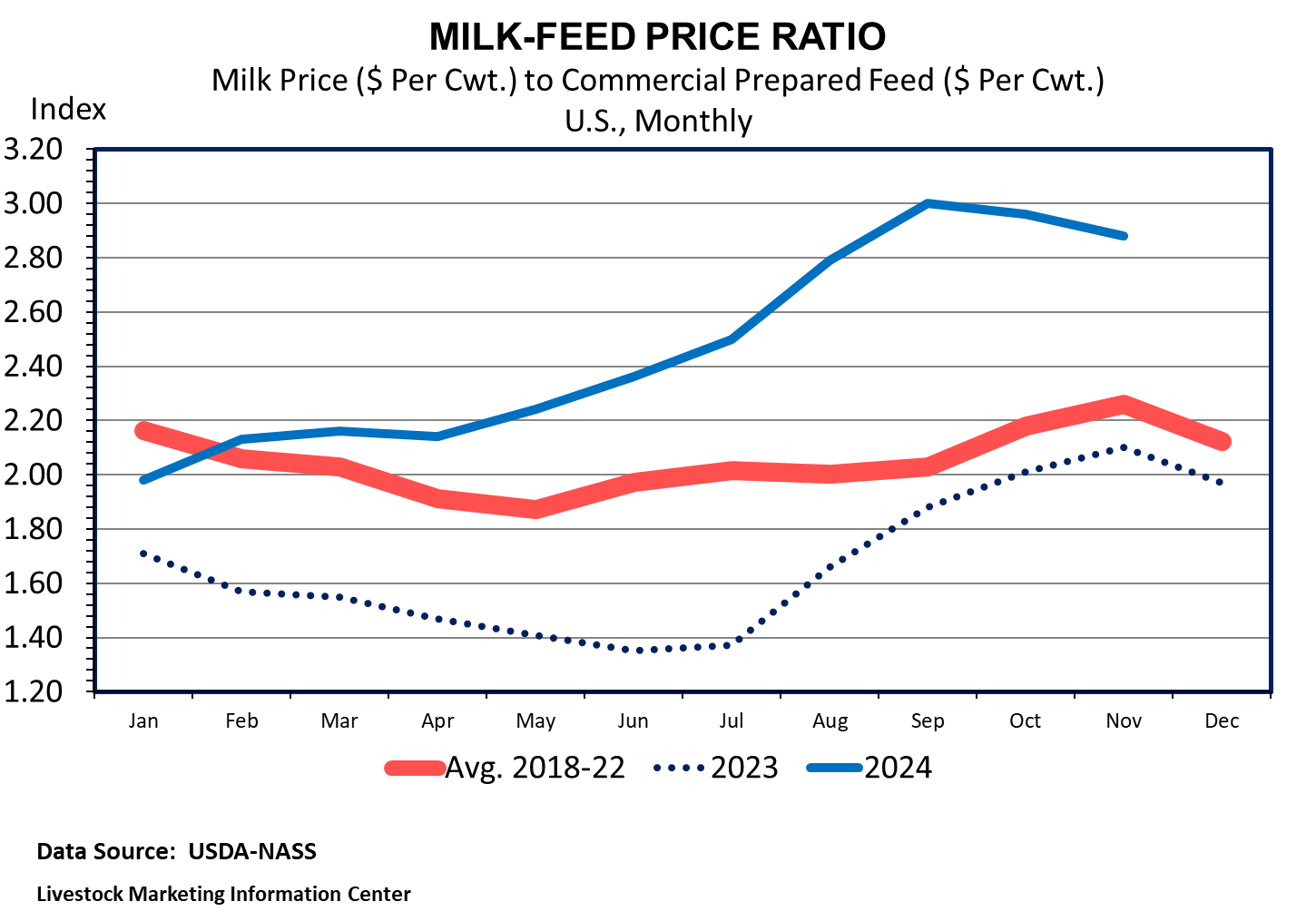

2024 in Review

Margins improved significantly in 2024 compared to 2023 (Figure 1). In 2024, U.S. milk production is estimated to be about even with 2023 production, according to the U.S. Department of Agriculture (USDA). Through October, milk production was down just 0.2% year over year. Those declines mostly occurred through the first half of the year. Through June, average daily production dropped by approximately 0.9%. Production since then has been up by around 0.2%. These production swings have been largely attributable to changes in the number of milk cows. After being lower than 2023 for most of the year, milk cow inventory exceeded year-ago figures in October 2024.

According to the USDA, Georgia milk production is up slightly through October 2024 (0.3% compared to the same period last year). However, milk producers in Georgia appear to have differed in their milk cow inventory decisions and their milk productivity. The average number of milk cows in Georgia in October 2024 was about 5% below 2023. However, improvements in milk production per cow in Georgia have been tremendous this year. Milk production per cow per day was down about 1% through the first half of 2024. However, in the July–October period, milk production per cow increased by over 6% year over year.

Dairy product production changes varied by product this year. Butter production increased by 6% through October. Total cheese production was roughly flat. In contrast, dry skim milk production declined by about 15%.

Inventory and production changes had significant impacts on prices in 2024. Butter prices have generally remained elevated compared to 2023, aside from the significant butter price rally in the fall of 2023 that was not matched in 2024, despite growing butter stocks. Cheddar cheese prices trended higher through 2024, seeing some strength in the summer and fall on falling inventories and lower production. Nonfat dry milk prices slumped for much of the year despite the lower production because of lagging demand. However, the end of the year saw nonfat dry milk and whey prices jump to prices not seen since 2022.

Year-over-year export demand was slightly stronger thanks to growth across multiple products. Through October, exports were up approximately 2% in 2024 compared to 2023 but still lag 2022’s impressive figures. Key growth markets include Mexico, Central America, and South America.

2025 Outlook

With milk production ramping up on higher cow inventory numbers, a key question in the year ahead is going to be where supply and demand balance. Should milk production continue to increase, milk prices will likely slide back from their current high levels. The USDA is projecting an all-milk price of $22.55 for 2025, about 10 cents below 2024’s estimated price.

The most significant headwinds may come from exports. With exports to China appearing to decline for yet another year in 2024, other partners would need to grow. However, trade policy and potential headwinds to global economic growth may impede that export growth.

HPAI may prove to be a wildcard in 2025. While HPAI has the potential to disrupt supplies (as seen in recent data from California), at its current prevalence, it appears that it has not been a significant drag on milk production at the national level. Additionally, while there were initial fears of reduced milk demand when news of HPAI broke in the spring of 2024, these did not materialize. This area will be an important one to watch through 2025 should this situation change.

Lastly, federal order reform could impact dairy producers in Georgia. Several changes are being recommended that will have industry-wide implications, such as the “higher of” calculation in the Class I skim milk price. Two areas to highlight for Georgia producers come from changes in milk composition factors and Class I differential changes. The update to milk composition factors will likely lead to higher milk prices in marketing orders that calculate prices on pounds of skim milk and butterfat, including the Appalachian, Southeast, and Florida orders that are important to Georgia dairy producers. The update to the Class I differentials would benefit much of the Southeast with significant Class I differential increases. These potential changes should be carefully monitored in milk markets this year.

Status and Revision History

In Review on Jan 15, 2025

Published on Jan 22, 2025