Main Takeaways

- The outlook in 2025 for the Georgia broiler industry is one of cautious optimism.

- The significant risk is market fundamentals—will production growth overshoot demand and cause prices to fall?

- Other areas to watch include relatively low exports, animal protein price competitiveness, and potential grower-contract regulations.

The upcoming year is forecast to be positive but risky for the broiler industry. Despite chicken production being forecast to increase moderately in 2025, chicken prices are expected to remain steady in the year ahead. This is thanks in part to the attractive position chicken has compared to other animal proteins. The risk in the year ahead is that production overshoots demand and prices fall. Other areas to watch are slumping exports and potential regulatory changes.

2024 in Review

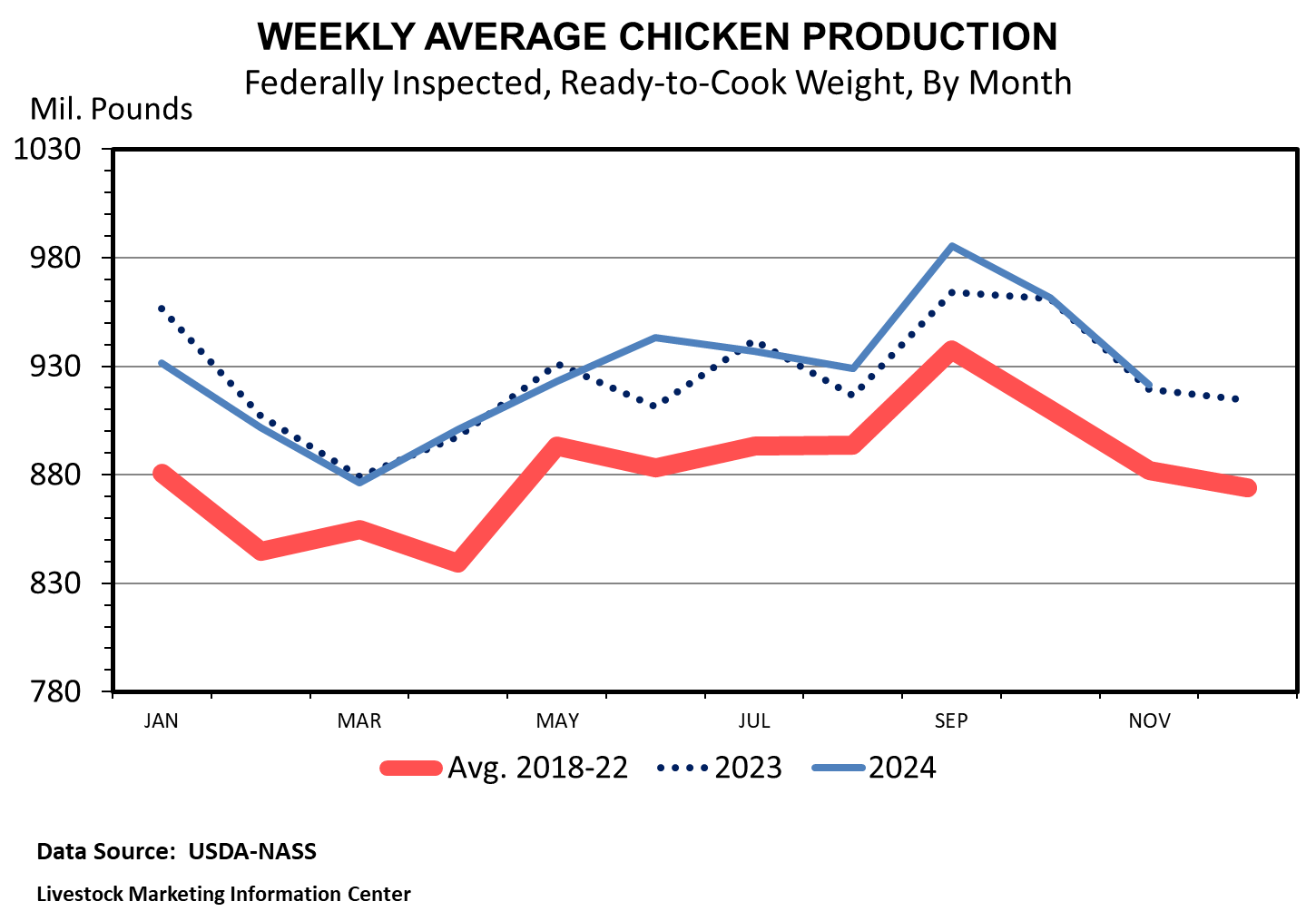

The U.S. Department of Agriculture (USDA) estimates that chicken production was up around 1.6% in 2024. This has come from a combination of higher slaughter numbers and heavier weights. Looking ahead, it is important to note that production varied significantly through the year (Figure 1). In the first half of 2024, ready-to-cook chicken production was down slightly. Importantly, from July to October, ready-to-cook chicken production was up 3.1% compared to the same period in 2023.

The USDA estimates that U.S. chicken disappearance (amount used for both fresh and processed meat sold through grocery stores and used in restaurants) exceeded 100 lb per person for the first time on record in 2024. This represents an increase of around 2.8% year over year. Amid mostly higher prices compared to 2023, higher consumption suggests strong demand for chicken.

However, while domestic demand exceeded expectations, exports lagged. In January 2024, USDA forecasted exports to be around 7.3 billion pounds. By December, the estimates for 2024 pegged chicken exports at roughly 6.7 billion pounds. This represents a decline of about 7.3% from initial forecasts and a 7.1% drop year over year. These are the lowest export figures since 2007 (aside from 2015, when highly pathogenic avian influenza [HPAI] caused export restrictions).

Prices in 2024 were much improved compared to 2023. With production in the first half of the year roughly in-line with 1-year-ago figures, but demand clearly increasing, chicken prices moved higher. Wholesale chicken breast, leg, leg quarters, and wing prices all exceeded year-ago levels for most of the year. However, there was some notable softness in breast and wing prices in the fall. These price moves are not abnormal given seasonal trends. Legs and leg quarters showed significant strength through the end of the year.

2025 Outlook

The fundamental risk to the 2025 outlook appears to be production increases outpacing demand. Looking back just a few years is illustrative: after significant production growth in 2022 (roughly 4% in the second half of 2022), reflecting a rebound from COVID-19 issues, prices plummeted at the end of 2022. These production levels were largely maintained in the first half of 2023 (up 2.9% year over year), extending the period of low prices through much of 2023. However, in late 2023 and into early 2024, supply and demand found a balance at higher prices on lower production and stronger demand in 2024.

Going into 2025, production appears to be ramping up again to similar year-over-year increases as seen in the previously discussed production increases at the end of 2024. Data for eggs set and chicks placed suggest that production increases will continue into at least the beginning of 2025. Additionally, while the number of layers is down significantly compared to 2023 and 2022, productivity is above last year by a wide margin and is similar to 2022. Lastly, the second half of 2024 saw an increase in the number of chicks hatched intended for U.S. placements into hatchery supply flocks. All of these data points suggest that production will be increasing through 2025. The USDA currently estimates a 1.4% increase in 2025.

Domestic demand risks appear low as chicken is very competitive with other animal proteins. Demand headwinds may come on the export front again in 2025. Increased competition from other exporting countries, such as Brazil, is likely to continue in the year ahead. Additionally, increased chicken production in key export destinations reduces demand for chicken from other countries. Exports may increase this year, but they are likely to remain at relatively low levels compared to recent history.

Lastly, regulatory changes may have a significant impact in the years ahead for the broiler industry. The USDA has proposed rules that would require changes to poultry grower contracts that could have implications for both growers and integrators. In particular, the proposed rule would implement a system in which growers would receive a minimum payment, rather than the current, more flexible tournament pay structure where grower pay varies up and down from a base pay rate. Any final rule would likely be contested, but it is an area to watch as it could affect grower and integrator interest in building new chicken houses now and in the future.

Status and Revision History

In Review on Jan 08, 2025

Published on Jan 22, 2025