Annual Publication

130-3-02

Main Takeaways

- Food price growth in 2025 is projected to align with inflation at around 2.5%, although prices for food consumed away from home are expected to remain higher than those for food consumed at home. Commodity prices are forecast to trend downward in the near term, with stability anticipated in the medium term.

- According to the most recent USDA farm income forecast, declining crop prices are expected to outweigh revenue gains from animal products, combined with slightly reduced input costs, leading to lower national net farm income in 2024.

- USDA projections indicate a decline in net farm income of 4.1% in nominal terms and 6.3% in inflation-adjusted terms nationally in 2024. However, these projections will not apply to Georgia because of the significant damages caused by Hurricane Helene, which resulted in lost output and infrastructure.

- Looking forward to 2025 and beyond, numerous geopolitical risks combined with various proposed policies—including tariffs and retaliation, immigration controls, tax policies, energy strategies, and inflation-targeted monetary policies—contribute to ongoing uncertainties surrounding U.S. and Georgia agricultural economic outcomes.

The consensus around the 2025 U.S. economic outlook suggests a slowdown in GDP growth relative to 2024. Moderate investment growth is expected along with stable labor markets (UGA Selig Center for Economic Growth; Federal Reserve; University of Michigan). Government expenditures are expected to grow, widening the fiscal deficit, and net exports are likely to trend downward because of concerns over federal debt servicing and the strong U.S. dollar, respectively. Major risks to economic growth and stability are policy uncertainty—tariffs and retaliation, tax policies, immigration controls, energy strategies, and inflation-targeted monetary policies, followed by numerous geopolitical risks encompassing major economies of the world in Europe, the Middle East, and others. Simultaneous implementation of many of the proposed policies may act in opposite directions, e.g., higher tariffs can offset tax incentives, creating additional uncertainties about economic outcomes.

U.S. Agricultural Economy

The USDA's annual U.S. agricultural outlook from Nov. 7, 2024, i.e., projections to 2034, indicates:

- a positive outlook on crop and livestock production volumes.

- Production is projected to grow among six of the eight major crops, including upland cotton, soybeans, wheat, corn, barley, and oats during the projection period (2025–2034). Declines are expected for rice and sorghum because of relative profitability. Much of the growth is attributable to rising yields because of technology and R&D.

- Production for all main animal products are expected to rise over the projection period, achieving record-high levels of production by the end of 2034 for all products except beef and turkey. Production growth, in percent terms, is projected to be near or above double digits for all products except turkey and eggs.

- a mixed outlook for prices: down for crop products and significantly up for animal products.

- 2025 prices of all crops are projected to remain well below recent highs, but may increase or decline modestly over the rest of the projection period (2026-2034).

- Nominal price changes for all animals and animal products are varied during the 2025–2034 projection period, with prices declining for several commodities (beef and hog) and rising for some (broiler, turkey, eggs, and milk).

- lower net returns for crops, but stabilizing over the next decade.

- Net returns (revenues minus variable costs) per acre are significantly lower during the projection period for all crops, after record levels in 2021 or 2022. This is because prices decline in the short term and then stabilize in the medium term.

- Rice returns are challenged by declining prices and acreage.

- an upward trend on export volumes for crops and animal products.

- U.S. crop exports are expected to remain steady or increase over the next decade. Corn, soybeans, wheat, rice, and upland cotton exports are expected to rise steadily over the projection period, but none are projected to reach record-high volumes. The most noteworthy increase is soybean oil exports with anticipated 181% growth during the projection period.

- All animal products experience some degree of export growth over the projection period (with exports of pork and eggs notably strong). Beef exports are projected to be relatively low in the early stages as cattle herd inventories are rebuilt, but then rise for most of the projection period. Chicken exports are projected to grow to a record high.

U.S. Farm Income

Separately, USDA also forecasts that farm sector income is expected to fall in the near term after reaching record highs in 2022. Net farm income, a broad measure of profits, is forecast at $140.7 billion in calendar year 2024, a decrease of $6.0 billion (4.1%) relative to 2023 in nominal (not adjusted for inflation) dollars. After adjusting for inflation, net farm income is forecast to decrease $9.5 billion (6.3%) in 2024 relative to 2023. Despite this expected decline, net farm income in 2024 would be 15.9% above its 20-year average (2004–23) of $121.4 billion.

Key changes between 2023 and 2024 include:

- Cash receipts from the sale of agricultural commodities are forecast to decrease by $4.0 billion (0.8%, in nominal terms) from 2023 to 2024. Total crop receipts are expected to decrease by $25.0 billion (9.2%) from 2023. In contrast, total animal/animal product receipts are expected to increase by $21.0 billion (8.4%).

- Government payments are expected to decline by $1.7 billion (13.6%) from 2023 to 2024.

- Total production expenses, including those associated with operator dwellings, are forecast to decrease by $8.0 billion (1.7%) from 2023 to 2024.

- Farm sector solvency is expected to be stronger, but liquidity to be weaker in 2024 relative to 2023 (slight improvement in debt-to-asset ratio, but working capital is down by 6.9%).

Georgia's Agricultural Economy

Agriculture, a driving force for local economies across Georgia, has long shaped the state’s history. In 2022, food and fiber production and related industries contributed more than 323,300 jobs and $83.6 billion in output to Georgia’s $1.4 trillion economy (2024 Ag Snapshots).

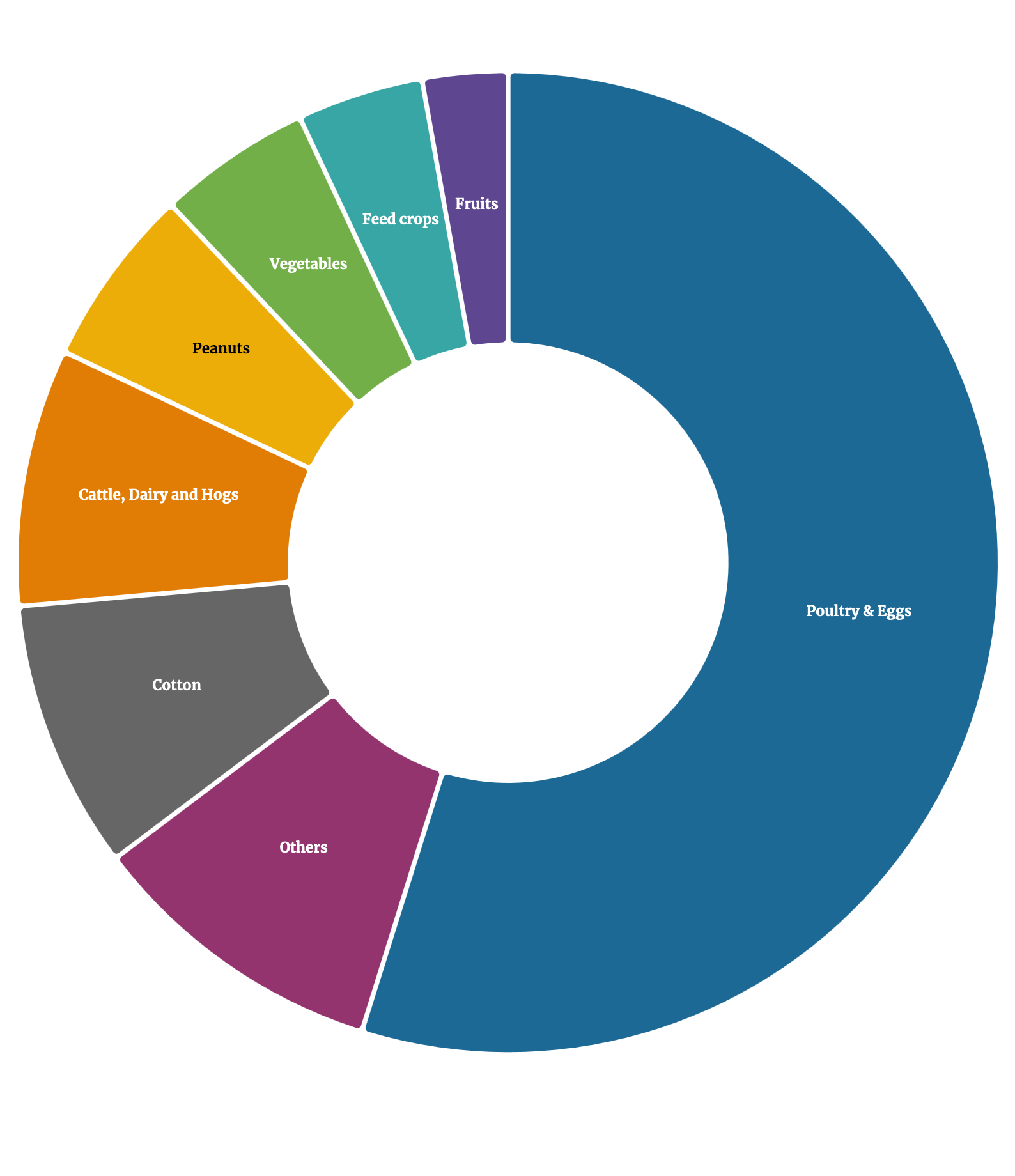

Figure 1. 2023 Georgia Cash Receipts ($12.5 billion).

Click on the chart to interact with this data.USDA reports detail the structure of Georgia’s agricultural economy:

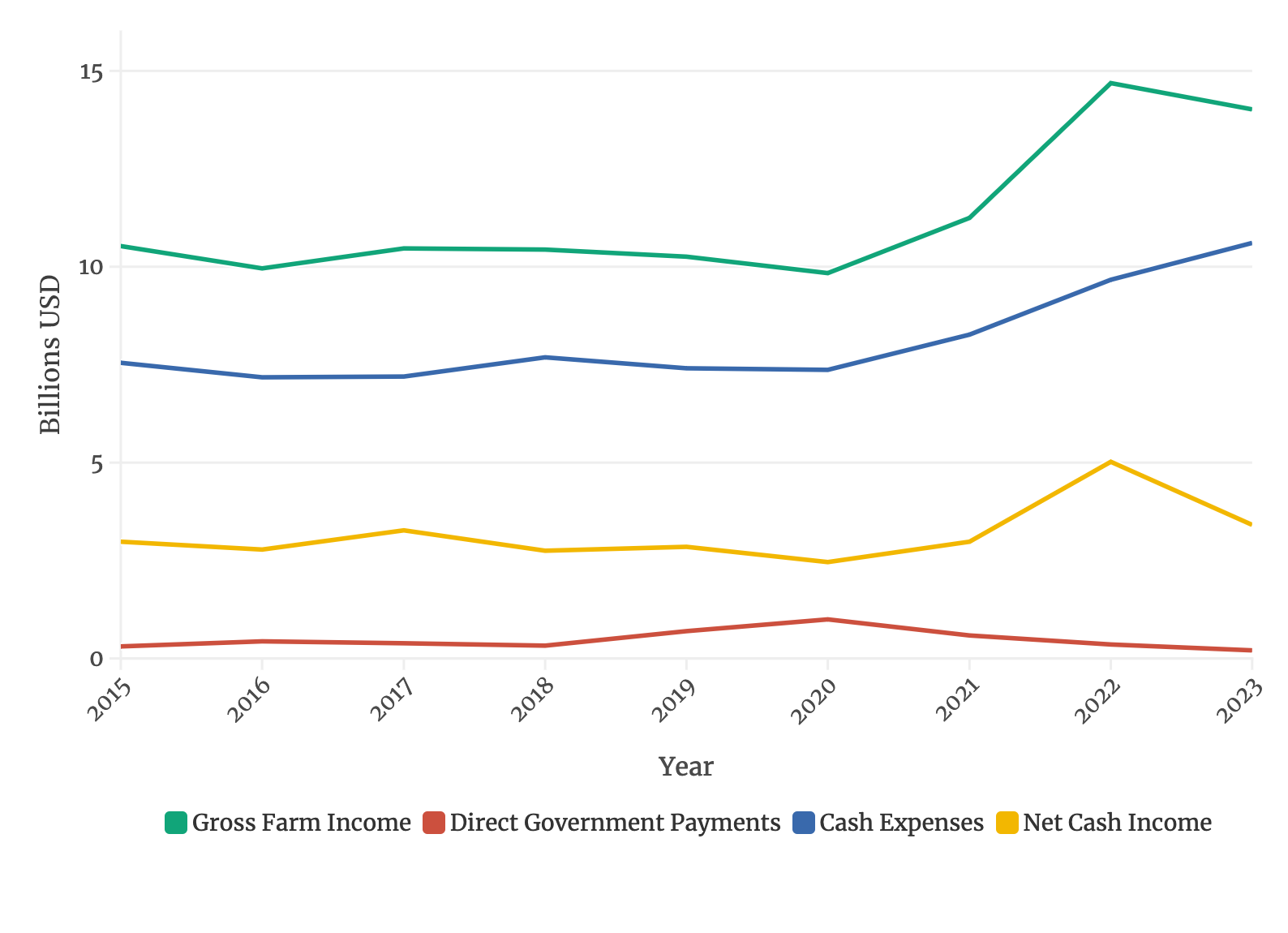

Figure 2. Georgia Farm Income, 2015–2023 (Billion $). Click on the chart to interact with this data.

Figure 2. Georgia Farm Income, 2015–2023 (Billion $). Click on the chart to interact with this data.

- Poultry and eggs, cotton, and peanuts account for 70% of Georgia’s cash receipts in 2023. Among states, Georgia ranks 17th in total cash receipts. Figure 1 shows the shares of broad commodity groups among Georgia’s total cash receipts.

- In addition to cash receipts, the USDA provides information on direct government payments, net cash expenses, and net cash income by state. Georgia’s net cash income is $3.4 billion in 2023, a $1.6 billion decrease from 2022. Among U.S. states, Georgia ranks 19th in net cash income. Figure 2 shows a constant gap between income and expenses, which widened during the COVID-19 pandemic. Since 2022, expenses went up (by $1 billion), but both gross and net cash income show sharp declines. Government payments also show a declining trend starting in 2020.

- Finally, according to the USDA, Georgia’ $3.86 billion in exports made the state the 18th largest exporter in 2022. Major export commodities are cotton, poultry and eggs, peanuts, fruits and vegetables, and tree nuts.

Georgia's 2025 Agricultural Economic Outlook

The broader U.S. economy is anticipated to experience a slowdown alongside a reduction in price inflation. Food price growth is expected to align with the overall inflation rate, though food consumed away from home is projected to remain relatively more expensive than food consumed at home. Commodity prices are trending downward, with expectations of stability in the medium term. However, a return to the record levels observed in 2021 and 2022 is not anticipated over the next decade, under normal circumstances.

Although the USDA does not provide state-specific projections for the farm economy, historical trends indicate a strong correlation between Georgia’s agriculture and national patterns in terms of revenue growth, and output and input prices. The most recent USDA farm income forecast suggests that falling crop prices are expected to outweigh gains in revenue from animal products, alongside slightly reduced input costs, resulting in a lower national net farm income for 2024. The USDA projects declines of 4.1% and 6.3% in nominal and inflation-adjusted net farm income, respectively.

However, these projections are not applicable to Georgia because of several factors, most notably the significant damage to agriculture and related industries in the Southeast caused by Hurricanes Helene and Debby. Damage estimates from Helene alone are placed at $5.6 billion, including nearly $0.9 billion in production infrastructure losses (UGA's Helene Report). Most commodities in Georgia—such as cotton, poultry, beef, dairy, and specialty crops like pecans, blueberries, vegetables, and nursery products—suffered substantial output losses because of Helene. With Congressional approval of disaster and economic assistance to agriculture, totaling $31 billion, the rapid delivery of aid is critical to Georgia’s farm community.

Without immediate disaster relief, the decline in national working capital (6.9%) is expected to be more pronounced in Georgia, potentially reversing solvency trends (debt-to-asset and debt-to-equity ratios). Farms with narrow profit margins and high labor costs are likely to face significant challenges in this environment.

Preliminary analysis from the University of Missouri's Food & Agricultural Policy Research Institute (FAPRI) indicates that midwestern states stand to gain most from the $10 billion allocated for economic assistance to crop producers. Additional information on the allocation of assistance for 2023 and 2024 disasters, budgeted at $21 billion, was not available at the time of this publication.

Looking Ahead to 2025 and Beyond

Various proposed policies are expected to influence agriculture in the United States and Georgia.

Tariffs and Retaliation

Agricultural exports are likely to be targeted if other countries retaliate against the proposed U.S. manufacturing tariffs by the incoming administration. Retaliatory tariffs during the last round resulted in a $27 billion reduction in U.S. agricultural exports, prompting market facilitation payments of approximately $23 billion to farmers.

The American Farm Bureau president has expressed concern over potential impacts; he said, “We don’t support tariffs ... other countries take it out on agriculture” (RadioIowa).

Immigration Controls

Specific details regarding proposed immigration controls are not yet available, making it difficult to assess their implications for labor availability and costs. However, labor shortages remain a critical concern, particularly in the agricultural sector.

Tax Policies

Proposed changes to corporate tax policies may have limited effects on U.S. farms, as 96% of them are family-owned enterprises (AgWeb.com).

Energy Strategies

Incentives for both traditional and green energy sources are expected to influence commodity prices.

Inflation and Monetary Policies

Concerns about inflation persist, and anticipated reductions in capital costs may not be realized (Federal Reserve).

As noted, some proposed policies may counteract each other, such as higher tariffs and a strong dollar offsetting compensatory payments, thereby increasing uncertainty around economic outcomes. Additionally, geopolitical risks involving major economies—including Europe and the Middle East—add to the unpredictability of agricultural input and output prices. However, consumer demand remains robust, particularly for animal protein, and is supported by a resilient U.S. economy.

Status and Revision History

In Review on Jan 08, 2025

Published on Jan 22, 2025