Introduction

The Dairy Business Analysis Project (DBAP) was initiated in 1996 by the University of Florida in an effort to measure and document the financial performance of Florida dairy farms using standardized accounting measures. The University of Georgia has been a formal collaborator since 1998. A committee of dairymen appointed by Southeast Milk, Inc. oversees the project and helps direct its course. The DBAP website is http://dairy.ifas.ufl.edu/dbap.

Financial data for the year 2005 were collected from participating dairy farms and screened for completeness and validity. Each dairy farm then received a benchmark report detailing its financial results compared to the average results for the other participants and the six dairy farms with the highest net farm income per cwt. This benchmark report is discussed with the dairy farms to identify challenges and opportunities for improvement.

This publication is a summary of the financial performance of the dairy farms that participated in 2005. It is intended for general use by dairy farmers, the allied industry, government, and educational professionals.

Results

Summary results are presented in Tables 1.1 to 4.4 and Figures 1 to 5. Revenues and expenses may not add up due to rounding. In brief, 21 dairy farms were included in the summary results. Of these, 15 were located in Florida and 6 in Georgia. The average herd size of the participating dairies was 1,045 cows and 538 heifers with 18,322 pounds of milk sold per cow. The average culling rate was 36 percent. The average milk price was $18.24. Average total revenues were $20.73 per cwt. milk sold. Total expenses averaged $20.20 per cwt. sold. The largest items were purchased feed, $7.22, and personnel costs, $3.50. Net farm income from operations averaged $0.53 per cwt. sold. Net farm income per cwt. was $0.07.

The herds were divided into three equal groups based on size, <446, 446 to 670 and >670 cows. The average number of cows and heifers by group was 261 cows and 50 heifers, 562 cows and 348 heifers, and 2,312 cows and 1,218 heifers. Milk sold per cow was 15,777, 19,225 and 19,963 pounds by group. Culling rates were highest (42 percent) for the smallest herd size and lowest (31 percent) for the largest herd size. Milk revenue increased with herd size ($17.95, $18.14 and $18.63 per cwt.) but total revenue was highest ($21.57 per cwt.) for the smallest herd size. Total expenses decreased with increasing herd size ($22.22, $20.75 and $17.65 per cwt.). This resulted in the highest net farm income from operations ($2.79 per cwt.) and net farm income ($2.79 per cwt.) for the largest herd size. The largest expense item was purchased feed for each group but it decreased with increasing herd size. Labor costs were highest for the smallest herd size and decreased with herd size.

The herds were divided into three equal groups on pounds of milk sold, <17,300, 17,300 to 19,500 and >19,500. The average pounds of milk sold, cow and heifer numbers for each group, was 14,950 pounds of milk, 1,117 cows and 363 heifers; 18,420 pounds of milk, 447 cows and 215 heifers and 21,594 pounds of milk, 1,571 cows and 1,038 heifers. Culling rates were highest for the lowest production group (44 percent) and lowest for the highest production group (29 percent). Milk revenue was nearly equal for each group ($18.32, $18.08, and $18.32 per cwt.) but total revenue was highest for the lowest yield group and lowest for the highest yield group. Total expenses decreased with increasing milk sold ($21.78, $19.86 and $18.98 per cwt.). This resulted in the highest net farm income from operations ($1.31 per cwt.) and net farm income ($1.19 per cwt.) for the highest production group.

Data Collection and Accounting Methods

Dairy farms in Florida and Georgia were asked to participate in DBAP. Participants were not a random sampling of all dairy farms in the two states. The financial performance results in this publication are therefore not necessarily representative of the results of all dairy farms in Florida and Georgia.

Most of the data were collected by extension agents when visiting dairy farms using a standardized data collection spreadsheet. Occasionally, data were sent in by the dairy farms. The financial data were either entered into the spreadsheet on the farm or mailed in on paper copies of the spreadsheet.

The accounting methods followed the recommendations made by the Farm Financial Standards Council (Farm Financial Standards Council. 1997. Financial Guidelines for Agricultural Producers.). All revenues and expenses were accrual adjusted. Cash receipts and expenses were therefore adjusted for changes in inventory, prepaid expenses, accounts payable, and accounts receivable. Depreciation data were often taken from tax records. Asset valuation was based on market values if available, but the changes from January 1 to December 31 were kept small. Unpaid management was valued at $50,000 per farm. Gain or loss on sale of purchased livestock resulted when depreciation did not completely account for the gain or loss in the value of the purchased livestock during 2005. Appreciation resulted when machinery and building depreciation did not completely account for the gain or loss in the value of these capital assets during 2005. The bottom line of each dairy farm is its net farm income. Net farm income is the return to the owner and unpaid family members for their labor, management, and equity in the dairy farm. It is the total income available for owner salary, new investments, taxes and paying off principal.

All submitted data were carefully scrutinized and checked for completeness. The cash flow statement reconciles the net cash flow resulting from the reported operating, investing, and financing activities with the reported available cash on the January 1 and December 31 balance sheets. The equity statement reconciles the changes in equity through reported retained capital and valuation with the calculated equity on the balance sheets. The reconciliation attempts typically resulted in unresolved imbalances. Both cash flow and equity imbalances had to be less than 10 percent to be included in the summary results reported here.

All results in this publication are the simple averages of the statistics of the dairy farms with valid data. Every dairy farm has equal weight. The simple average milk yield per cow is (17,000 + 19,000) / 2 = 18,000 lbs. / cow.

Some definitions and calculation rules are as follows:

Asset turnover ratio = total revenues / average assets

Assets = value of assets on the balance sheet

Average assets = average of value of assets on January 1 and December 31

Average equity = average of value of equity on January 1 and December 31

Capital replacement and term debt repayment margin = NFIFO + depreciation + interest on term debt – net social security and income taxes – owner withdrawals – annual scheduled payments on term debt and capital leases.

Cash flow coverage ratio = (cash revenues – cash expenses) / current liabilities

Current assets = short-term assets that can be utilized within one year

Current liabilities = liabilities due within one year

Current ratio = current assets / current liabilities

Debt to asset ratio = liabilities / assets

Debt to equity ratio = liabilities / equity

Depreciation expense ratio = depreciation / total revenue

Equity = assets - liabilities

Equity to asset ratio = equity / assets

FTE = full time equivalent worker, on average 54 hours per week

Interest expense ratio = interest paid / total revenue

Liabilities = value of liabilities on the balance sheet

Net farm income = NFIFO + gain on sale of capital assets

NFIFO = net farm income from operations

NFIFO ratio = NFIFO / total revenue

Operating expense ratio = (total operating expenses – depreciation) / total revenue

Operating profit margin ratio = (NFIFO + interest paid – unpaid management) / total revenues

Rate of return on dairy assets = (NFIFO + interest paid – unpaid management) / average assets

Rate of return on equity = (NFIFO – unpaid management) / average equity

Std = standard deviation

Term debt and capital lease coverage ratio = (NFIFO + non dairy income + depreciation + interest paid on term debt – net social security and income taxes – owner withdrawals) / (annual scheduled payments on term debt and capital leases).

Working capital = current assets - current liabilities

Tables

| Table 1.1. DBAP 2005 Summary - Business size and production efficiency by state and overall average, median, and standard deviation. | |||||

|

|

Overall |

State Averages |

|||

| Category |

Average |

Median |

Std1 |

Florida |

Georgia |

|

Number of farms |

21 |

21 |

21 |

15 |

6 |

| Business Size: |

|

|

|

|

|

|

Average number of cows |

1,045 |

575 |

1,157 |

1,155 |

770 |

|

Average number of heifers |

538 |

290 |

720 |

543 |

527 |

|

Milk sold (million lb) |

20.21 |

10.99 |

22.96 |

21.53 |

16.94 |

|

FTE2 workers |

19 |

12 |

17 |

20 |

16 |

|

Acres of pasture + cultivated land |

569 |

320 |

732 |

633 |

410 |

|

|

|

|

|

|

|

| Production Efficiency: |

|

|

|

|

|

|

Milk sold (lb / cow / year) |

18,322 |

18,168 |

3,237 |

17,659 |

19,979 |

|

Cows / FTE worker |

51 |

52 |

25 |

55 |

40 |

|

Milk sold / FTE worker (million lb) |

0.93 |

0.94 |

0.44 |

0.97 |

0.82 |

|

Cull rate |

36% |

32% |

21% |

31% |

47% |

2 Full-time equivalent

| Table 1.2. DBAP 2005 Summary - Revenues and expenses by state and overall average, median, and standard deviation ($/cwt.). | |||||

|

|

Overall |

State Averages |

|||

|

Category |

Average |

Median |

Std1 |

Florida |

Georgia |

|

Number of farms |

21 |

21 |

21 |

15 |

6 |

|

Revenues: |

|

|

|

|

|

|

Milk sold |

18.24 |

18.28 |

0.62 |

18.38 |

17.89 |

|

Raised, leased cow sales |

0.89 |

0.33 |

1.41 |

0.60 |

1.62 |

|

Heifer sales |

0.45 |

0.36 |

0.44 |

0.50 |

0.33 |

|

Gain on purchased livestock sales |

(0.13) |

(0.06) |

0.83 |

(0.37) |

0.48 |

|

Other revenues |

1.28 |

0.78 |

1.45 |

1.30 |

1.23 |

|

Total Revenues |

20.73 |

20.24 |

2.21 |

20.41 |

21.55 |

|

Expenses: |

|

|

|

|

|

|

Personnel |

3.50 |

3.08 |

1.42 |

3.43 |

3.69 |

|

Purchased feed |

7.22 |

6.81 |

2.33 |

7.96 |

5.36 |

|

Crops |

0.41 |

0.13 |

0.59 |

0.34 |

0.58 |

|

Machinery |

1.11 |

1.00 |

0.75 |

1.18 |

0.94 |

|

Livestock |

2.01 |

1.92 |

0.90 |

1.99 |

2.06 |

|

Milk marketing |

1.22 |

1.30 |

0.24 |

1.19 |

1.32 |

|

Buildings and land |

0.74 |

0.44 |

1.01 |

0.52 |

1.30 |

|

Interest |

0.67 |

0.56 |

0.61 |

0.69 |

0.61 |

|

Depreciation: |

|

|

|

|

|

|

Livestock |

1.11 |

0.97 |

1.07 |

1.11 |

1.12 |

|

Machinery |

0.81 |

0.40 |

0.85 |

0.76 |

0.95 |

|

Buildings |

0.39 |

0.25 |

0.42 |

0.37 |

0.44 |

|

Other expenses |

1.01 |

1.03 |

0.38 |

1.06 |

0.89 |

|

Total Expenses: |

20.20 |

18.73 |

3.80 |

20.59 |

19.25 |

|

Net farm income from operations |

0.53 |

0.84 |

3.20 |

(0.18) |

2.30 |

|

Gain on sale of capital assets |

(0.46) |

0.00 |

1.37 |

(0.03) |

(1.56) |

|

Net Farm Income |

0.07 |

0.84 |

3.54 |

(0.20) |

0.74 |

| Table 1.3. DBAP 2005 Summary - Financial performance by state and overall average, median, and standard deviation. | |||||

|

|

Overall |

State Averages |

|||

|

Category |

Average |

Median |

Std1 |

Florida |

Georgia |

|

Number of farms |

21 |

21 |

21 |

15 |

6 |

|

Liquidity: |

|

|

|

|

|

|

Current ratio |

5.78 |

0.61 |

17.47 |

1.53 |

16.42 |

|

Working capital ($) |

123,069 |

21,375 |

673,678 |

(23,839) |

490,338 |

|

Solvency: |

|

|

|

|

|

|

Debt to asset ratio |

0.39 |

0.34 |

0.26 |

0.40 |

0.38 |

|

Equity to asset ratio |

0.61 |

0.66 |

0.26 |

0.60 |

0.62 |

|

Debt to Equity Ratio2 |

2.47 |

0.52 |

5.88 |

1.75 |

4.26 |

|

Profitability: |

|

|

|

|

|

|

Rate of return on assets |

0.04 |

0.04 |

0.10 |

0.03 |

0.09 |

|

Rate of return on equity |

0.02 |

0.02 |

0.35 |

(0.06) |

0.24 |

|

Operating Profit Margin Ratio |

0.02 |

0.03 |

0.17 |

(0.01) |

0.08 |

|

Financial efficiency: |

|

|

|

|

|

|

Asset turnover rate |

0.78 |

0.81 |

0.37 |

0.80 |

0.71 |

|

Operating expense ratio |

0.83 |

0.84 |

0.15 |

0.86 |

0.75 |

|

Depreciation expense ratio |

0.11 |

0.10 |

0.06 |

0.11 |

0.11 |

|

Interest expense ratio |

0.03 |

0.03 |

0.03 |

0.03 |

0.03 |

|

NFIFO Ratio3 |

0.03 |

0.04 |

0.15 |

(0.01) |

0.10 |

|

Repayment capacity: |

|

|

|

|

|

|

Cash flow coverage ratio |

5.96 |

0.58 |

19.28 |

0.71 |

19.08 |

|

Term debt coverage ratio4 |

2.90 |

0.42 |

7.30 |

3.77 |

0.72 |

|

Capital Replacement Margin5 ($) |

321,516 |

69,895 |

971,525 |

193,709 |

641,032 |

2 One dairy farm had negative equity.

3 Net farm income from operations ratio.

4 Term debt and capital lease coverage ratio.

5 Capital replacement and term debt repayment margin.

| Table 1.4. DBAP 2005 Summary - Balance sheet by state and overall average, median, and standard deviation ($/cow). | |||||

|

|

Overall |

State Averages |

|||

|

Category |

Average |

Median |

Std1 |

Florida |

Georgia |

|

Number of farms |

21 |

21 |

21 |

15 |

6 |

|

Balance Sheet (January 1): |

|

|

|

|

|

|

Current assets |

428 |

306 |

268 |

316 |

709 |

|

Total Assets |

6,800 |

4,176 |

5,763 |

5,502 |

10,044 |

|

Current liabilities |

507 |

408 |

379 |

581 |

324 |

|

Total Liabilities |

1,810 |

1,825 |

1,163 |

1,668 |

2,164 |

|

Equity |

4,990 |

2,415 |

6,108 |

3,834 |

7,880 |

|

Balance Sheet (December 31): |

|

|

|

|

|

|

Current assets |

487 |

368 |

317 |

425 |

641 |

|

Total Assets |

6,668 |

4,733 |

5,315 |

5,365 |

9,925 |

|

Current liabilities |

386 |

344 |

414 |

521 |

49 |

|

Total Liabilities |

1,896 |

1,914 |

1,159 |

1,854 |

2,001 |

| Equity |

4,772 |

2,657 |

5,724 |

3,511 |

7,924 |

| Table 2.1. DBAP 2005 Summary - Business size and production efficiency by average number of cows and milk per cow. | ||||||

|

|

Average number of cows |

Milk yield (lbs / cow / year) |

||||

|

Category |

< 446 |

446-670 |

> 670 |

< 17,300 |

17,300-19,500 |

> 19,500 |

|

Number of farms |

7 |

7 |

7 |

7 |

7 |

7 |

|

Business Size: |

|

|

|

|

|

|

|

Average number of cows |

261 |

562 |

2,312 |

1,117 |

447 |

1,571 |

|

Average number of heifers |

50 |

348 |

1,218 |

363 |

215 |

1,038 |

|

Milk sold (million lb) |

4.24 |

10.86 |

45.54 |

17.84 |

8.29 |

34.51 |

|

FTE workers |

7 |

14 |

36 |

15 |

9 |

33 |

|

Acres of pasture + cultivated land |

142 |

397 |

1,169 |

613 |

298 |

798 |

|

|

|

|

|

|

|

|

|

Production Efficiency: |

|

|

|

|

|

|

|

Milk sold (lb / cow / year) |

15,777 |

19,225 |

19,963 |

14,950 |

18,420 |

21,594 |

|

Cows / FTE worker |

37 |

49 |

66 |

58 |

47 |

47 |

|

Milk sold / FTE worker (million lb) |

0.59 |

0.93 |

1.26 |

0.89 |

0.88 |

1.02 |

|

Cull rate |

42% |

34% |

31% |

44% |

34% |

29% |

| Table 2.2. DBAP 2005 Summary - Revenues and expenses by average number of cows and milk per cow ($/cwt.) | ||||||

|

|

Average number of cows |

Milk yield (lbs / cow / year) |

||||

|

Category |

< 446 |

446-670 |

> 670 |

< 17,300 |

17,300-19,500 |

> 19,500 |

|

Number of farms |

7 |

7 |

7 |

7 |

7 |

7 |

|

Revenues: |

|

|

|

|

|

|

|

Milk sold |

17.95 |

18.14 |

18.63 |

18.32 |

18.08 |

18.32 |

|

Raised, leased cow sales |

1.08 |

0.96 |

0.63 |

1.47 |

0.37 |

0.84 |

|

Heifer sales |

0.38 |

0.34 |

0.64 |

0.37 |

0.36 |

0.63 |

|

Gain on purchased livestock sales |

0.14 |

(0.46) |

(0.07) |

0.07 |

(0.43) |

(0.03) |

|

Other revenues |

2.01 |

1.22 |

0.61 |

2.23 |

1.08 |

0.52 |

|

Total Revenues |

21.57 |

20.20 |

20.44 |

22.46 |

19.46 |

20.29 |

|

Expenses: |

|

|

|

|

|

|

|

Personnel |

4.04 |

3.63 |

2.85 |

3.31 |

3.96 |

3.24 |

|

Purchased feed |

7.31 |

7.36 |

6.99 |

7.92 |

7.28 |

6.46 |

|

Crops |

0.29 |

0.72 |

0.22 |

0.37 |

0.32 |

0.54 |

|

Machinery |

0.95 |

1.53 |

0.85 |

0.93 |

1.04 |

1.35 |

|

Livestock |

2.16 |

1.92 |

1.96 |

2.23 |

1.91 |

1.89 |

|

Milk marketing |

1.34 |

1.06 |

1.27 |

1.29 |

1.17 |

1.22 |

|

Buildings and land |

1.37 |

0.57 |

0.29 |

1.00 |

0.96 |

0.27 |

|

Interest |

0.93 |

0.52 |

0.55 |

0.93 |

0.45 |

0.61 |

|

Depreciation: |

|

|

|

|

|

|

|

Livestock |

1.67 |

0.67 |

0.99 |

1.70 |

0.92 |

0.71 |

|

Machinery |

0.88 |

1.14 |

0.42 |

0.63 |

0.75 |

1.05 |

|

Buildings |

0.23 |

0.53 |

0.41 |

0.41 |

0.09 |

0.66 |

|

Other expenses |

1.05 |

1.12 |

0.86 |

1.05 |

1.00 |

0.98 |

|

Total Expenses |

22.22 |

20.75 |

17.65 |

21.78 |

19.86 |

18.98 |

|

Net farm income from operations |

(0.65) |

(0.55) |

2.79 |

0.68 |

(0.40) |

1.31 |

|

Gain on sale of capital assets |

(1.23) |

(0.17) |

0.00 |

(0.50) |

(0.77) |

(0.12) |

|

Net Farm Income |

(1.88) |

(0.72) |

2.79 |

0.18 |

(1.17) |

1.19 |

| Table 2.3. DBAP 2005 Summary - Financial performance by average number of cows and milk per cow. | ||||||

|

|

Average number of cows |

Milk yield (lbs / cow / year) |

||||

| Category |

< 446 |

446-670 |

> 670 |

< 17,300 |

17,300-19,500 |

> 19,500 |

| Number of farms |

7 |

7 |

7 |

7 |

7 |

7 |

| Liquidity: |

|

|

|

|

|

|

|

Current ratio |

0.46 |

12.66 |

4.22 |

1.77 |

0.41 |

15.16 |

|

Working capital ($) |

24,649 |

7,679 |

336,879 |

207,250 |

(32,694) |

194,650 |

| Solvency: |

|

|

|

|

|

|

|

Debt to asset ratio |

0.48 |

0.30 |

0.40 |

0.38 |

0.43 |

0.36 |

|

Equity to asset ratio |

0.52 |

0.70 |

0.60 |

0.62 |

0.57 |

0.64 |

|

Debt to Equity Ratio1 |

5.99 |

0.65 |

0.77 |

0.79 |

5.92 |

0.70 |

| Profitability: |

|

|

|

|

|

|

|

Rate of return on assets |

(0.01) |

(0.01) |

0.15 |

0.04 |

(0.00) |

0.09 |

|

Rate of return on equity |

(0.08) |

(0.05) |

0.20 |

0.02 |

(0.07) |

0.12 |

|

Operating Profit Margin Ratio |

(0.08) |

(0.02) |

0.15 |

0.01 |

(0.04) |

0.08 |

| Financial efficiency: |

|

|

|

|

|

|

|

Asset turnover rate |

0.74 |

0.67 |

0.93 |

0.77 |

0.83 |

0.73 |

|

Operating expense ratio |

0.86 |

0.89 |

0.75 |

0.81 |

0.90 |

0.79 |

|

Depreciation expense ratio |

0.13 |

0.11 |

0.09 |

0.12 |

0.09 |

0.12 |

|

Interest expense ratio |

0.04 |

0.03 |

0.03 |

0.04 |

0.02 |

0.03 |

|

NFIFO Ratio2 |

(0.03) |

(0.02) |

0.13 |

0.03 |

(0.02) |

0.06 |

|

Repayment capacity: |

|

|

|

|

|

|

|

Cash flow coverage ratio |

0.15 |

13.03 |

4.68 |

0.57 |

0.74 |

16.56 |

| Term debt coverage ratio3 |

0.53 |

1.49 |

6.67 |

5.11 |

1.30 |

2.28 |

| Capital Replacement Margin4 ($) |

(1,170) |

69,793 |

895,924 |

342,885 |

35,085 |

586,576 |

2 Net farm income from operations ratio.

3 Term debt and capital lease coverage ratio.

4 Capital replacement and term debt repayment margin.

| Table 2.4. DBAP 2005 Summary - Balance sheet by average number of cows and milk per cow ($/cow). | ||||||

|

|

Average number of cows |

Milk yield (lbs / cow / year) |

||||

|

Category |

< 446 |

446-670 |

> 670 |

< 17,300 |

17,300- |

> 19,500 |

|

Number of farms |

7 |

7 |

7 |

7 |

7 |

7 |

|

Balance Sheet (January 1): |

|

|

|

|

|

|

|

Current assets |

336 |

350 |

599 |

334 |

291 |

660 |

|

Total Assets |

8,343 |

7,651 |

4,405 |

5,512 |

6,846 |

8,042 |

|

Current liabilities |

471 |

453 |

599 |

491 |

547 |

484 |

|

Total Liabilities |

1,877 |

1,604 |

1,949 |

1,858 |

1,374 |

2,197 |

|

Equity |

6,466 |

6,047 |

2,457 |

3,654 |

5,471 |

5,844 |

|

Balance Sheet (December 31): |

|

|

|

|

|

|

|

Current assets |

374 |

311 |

775 |

541 |

242 |

676 |

|

Total Assets |

8,526 |

6,726 |

4,751 |

5,715 |

7,017 |

7,271 |

|

Current liabilities |

223 |

304 |

631 |

410 |

259 |

490 |

|

Total Liabilities |

2,061 |

1,623 |

2,004 |

2,015 |

1,504 |

2,169 |

|

Equity |

6,465 |

5,102 |

2,747 |

3,700 |

5,513 |

5,102 |

| Table 3.1. DBAP 2005 Summary - Business size and production efficiency by net farm income per cwt. and rate of return on assets. | ||||||

|

|

Net farm income ($ / cwt.) |

Rate of return on assets (%) |

||||

|

Category |

< $(1.13) |

$(1.13) -$2.30 |

> $2.30 |

< (3)% |

(3)% - 9.5% |

>9.5% |

| Number of farms |

7 |

7 |

7 |

8 |

6 |

7 |

|

Business Size: |

|

|

|

|

|

|

|

Average number of cows |

591 |

523 |

2,022 |

580 |

435 |

2,100 |

|

Average number of heifers |

373 |

198 |

1,044 |

329 |

161 |

1,101 |

|

Milk sold (million lb) |

11.63 |

9.70 |

39.32 |

11.31 |

8.02 |

40.85 |

|

FTE workers |

15 |

10 |

32 |

14 |

9 |

33 |

|

Acres of pasture + cultivated land |

653 |

273 |

782 |

572 |

304 |

795 |

|

|

|

|

|

|

|

|

|

Production Efficiency: |

|

|

|

|

|

|

|

Milk sold (lb / cow / year) |

17,549 |

18,283 |

19,133 |

17,603 |

17,734 |

19,646 |

|

Cows / FTE worker |

37 |

55 |

61 |

39 |

47 |

67 |

|

Milk sold / FTE worker (million lb) |

0.65 |

1.00 |

1.13 |

0.70 |

0.83 |

1.27 |

|

Cull rate |

33% |

32% |

43% |

34% |

45% |

31% |

| Table 3.2. DBAP 2005 Summary - Revenues and expenses by net farm income per cwt. and rate of return on assets ($/cwt.). | ||||||

|

|

Net farm income ($ / cwt.) |

Rate of return on assets (%) |

||||

|

Category |

<$(1.13) |

$(1.13)- $2.30 |

> $2.30 |

<3% |

(3)% - |

>9.5% |

|

Revenues: |

|

|

|

|

|

|

|

Milk sold |

18.14 |

18.17 |

18.42 |

18.08 |

17.97 |

18.66 |

|

Raised, leased cow sales |

0.95 |

0.25 |

1.47 |

0.83 |

1.13 |

0.76 |

|

Heifer sales |

0.44 |

0.33 |

0.58 |

0.48 |

0.26 |

0.58 |

|

Gain on purchased livestock sales |

(0.48) |

(0.22) |

0.30 |

(0.62) |

0.46 |

(0.07) |

|

Other revenues |

2.27 |

0.84 |

0.72 |

2.03 |

1.00 |

0.66 |

|

Total Revenues |

21.33 |

19.38 |

21.49 |

20.80 |

20.81 |

20.59 |

|

Expenses: |

|

|

|

|

|

|

|

Personnel |

4.60 |

3.11 |

2.80 |

4.48 |

3.13 |

2.70 |

|

Purchased feed |

8.38 |

7.24 |

6.04 |

8.29 |

6.25 |

6.83 |

|

Crops |

0.51 |

0.27 |

0.45 |

0.44 |

0.51 |

0.28 |

|

Machinery |

1.56 |

0.84 |

0.94 |

1.43 |

0.95 |

0.88 |

|

Livestock |

1.97 |

2.02 |

2.05 |

1.96 |

2.01 |

2.07 |

|

Milk marketing |

1.27 |

1.11 |

1.30 |

1.19 |

1.26 |

1.23 |

|

Buildings and land |

1.14 |

0.67 |

0.42 |

1.00 |

0.93 |

0.29 |

|

Interest |

0.91 |

0.60 |

0.49 |

0.89 |

0.67 |

0.40 |

|

Depreciation: |

|

|

|

|

|

|

|

Livestock |

1.05 |

0.90 |

1.39 |

1.11 |

1.40 |

0.87 |

|

Machinery |

1.15 |

0.78 |

0.52 |

1.03 |

1.04 |

0.37 |

|

Buildings |

0.54 |

0.21 |

0.42 |

0.47 |

0.34 |

0.33 |

|

Other expenses |

1.22 |

1.04 |

0.77 |

1.22 |

0.87 |

0.89 |

|

Total Expenses |

24.27 |

18.77 |

17.57 |

23.51 |

19.37 |

17.14 |

|

Net farm income from operations |

(2.94) |

0.60 |

3.92 |

(2.71) |

1.44 |

3.45 |

|

Gain on sale of capital assets |

(0.94) |

0.00 |

(0.46) |

(0.82) |

(0.53) |

0.00 |

|

Net Farm Income |

(3.87) |

0.61 |

3.47 |

(3.53) |

0.91 |

3.45 |

| Table 3.3. DBAP 2005 Summary - Financial performance by net farm income per cwt. and rate of return on assets. | ||||||

|

|

Net farm income ($ / cwt.) |

Rate of return on assets (%) |

||||

|

Category |

< $(1.13) |

$(1.13) -$2.30 |

> $2.30 |

< (3)% |

(3)% - 9.5% |

>9.5% |

| Number of farms |

7 |

7 |

7 |

8 |

6 |

7 |

|

Liquidity: |

|

|

|

|

|

|

|

Current ratio |

1.02 |

12.16 |

4.17 |

0.99 |

13.96 |

4.25 |

|

Working capital ($) |

(307,705) |

24,654 |

652,257 |

(275,332) |

74,306 |

620,181 |

|

Solvency: |

|

|

|

|

|

|

|

Debt to asset ratio |

0.39 |

0.45 |

0.34 |

0.41 |

0.44 |

0.33 |

|

Equity to asset ratio |

0.61 |

0.55 |

0.66 |

0.59 |

0.56 |

0.67 |

|

Debt to Equity Ratio1 |

2.90 |

3.94 |

0.57 |

2.70 |

4.38 |

0.57 |

|

Profitability: |

|

|

|

|

|

|

|

Rate of return on assets |

(0.06) |

0.03 |

0.16 |

(0.06) |

0.03 |

0.17 |

|

Rate of return on equity |

(0.27) |

0.10 |

0.24 |

(0.25) |

0.13 |

0.25 |

| Operating Profit Margin Ratio |

(0.17) |

0.03 |

0.18 |

(0.15) |

0.05 |

0.18 |

|

Financial efficiency: |

|

|

|

|

|

|

|

Asset turnover rate |

0.55 |

0.90 |

0.89 |

0.57 |

0.82 |

0.98 |

|

Operating expense ratio |

0.97 |

0.84 |

0.69 |

0.96 |

0.78 |

0.74 |

|

Depreciation expense ratio |

0.13 |

0.10 |

0.10 |

0.13 |

0.13 |

0.08 |

|

Interest expense ratio |

0.04 |

0.03 |

0.02 |

0.04 |

0.03 |

0.02 |

| NFIFO Ratio2 |

(0.14) |

0.03 |

0.18 |

(0.13) |

0.06 |

0.17 |

|

Repayment capacity: |

|

|

|

|

|

|

|

Cash flow coverage ratio |

0.08 |

13.12 |

4.67 |

0.23 |

14.84 |

4.89 |

|

Term Debt Coverage Ratio3 |

1.26 |

0.82 |

6.61 |

1.21 |

0.48 |

6.90 |

|

Capital Replacement Margin4 ($) |

(324,083) |

60,030 |

1,228,600 |

(291,751) |

74,639 |

1,234,001 |

2 Net farm income from operations ratio.

3 Term debt and capital lease coverage ratio.

4 Capital replacement and term debt repayment margin.

| Table 3.4. DBAP 2005 Summary - Balance sheet by net farm income per cwt. and rate of return on assets ($/cow). | ||||||

|

|

Net farm income ($ / cwt.) |

Rate of return on assets (%) |

||||

|

Category |

< $(1.13) |

$(1.13) -$2.30 |

> $2.30 |

< (3)% |

(3)% - 9.5% |

>9.5% |

|

Number of farms |

7 |

7 |

7 |

8 |

6 |

7 |

|

Balance Sheet (January 1): |

|

|

|

|

|

|

|

Current assets |

337 |

302 |

646 |

330 |

428 |

541 |

|

Total Assets |

10,601 |

4,794 |

5,004 |

9,766 |

6,119 |

3,993 |

|

Current liabilities |

570 |

506 |

446 |

535 |

543 |

446 |

|

Total Liabilities |

1,930 |

1,828 |

1,671 |

1,950 |

1,982 |

1,502 |

|

Equity |

8,672 |

2,966 |

3,332 |

7,816 |

4,137 |

2,491 |

|

Balance Sheet (December 31): |

|

|

|

|

|

|

|

Current assets |

288 |

340 |

831 |

288 |

486 |

714 |

|

Total Assets |

9,884 |

4,634 |

5,486 |

9,153 |

5,952 |

4,441 |

|

Current liabilities |

468 |

294 |

397 |

457 |

222 |

446 |

|

Total Liabilities |

2,078 |

1,791 |

1,819 |

2,106 |

2,017 |

1,553 |

|

Equity |

7,806 |

2,843 |

3,666 |

7,048 |

3,935 |

2,888 |

| Table 4.1. DBAP 2005 Summary - Business size and production efficiency by assets per cow and liabilities per cow. | ||||||

|

|

Assets ($ / cow) |

Liabilities ($ / cow) |

||||

|

Category |

< $4,000 |

$4,000-$5,600 |

> $5,600 |

< $1,340 |

$1,340-$2,500 |

> $2,500 |

|

Number of farms |

7 |

7 |

7 |

7 |

7 |

7 |

|

Business Size: |

|

|

|

|

|

|

|

Average number of cows |

1,167 |

1,331 |

638 |

1,212 |

1,049 |

874 |

|

Average number of heifers |

710 |

471 |

434 |

886 |

142 |

588 |

|

Milk sold (million lb) |

22.87 |

24.49 |

13.28 |

24.24 |

17.69 |

18.71 |

|

FTE workers |

22 |

18 |

17 |

27 |

14 |

17 |

|

Acres of pasture + cultivated land |

426 |

558 |

725 |

608 |

424 |

677 |

|

|

|

|

|

|

|

|

|

Production Efficiency: |

|

|

|

|

|

|

|

Milk sold (lb / cow / year) |

17,947 |

18,535 |

18,483 |

19,077 |

17,549 |

18,339 |

|

Cows / FTE worker |

52 |

66 |

34 |

45 |

65 |

43 |

|

Milk sold / FTE worker (million lb) |

0.93 |

1.20 |

0.65 |

0.85 |

1.10 |

0.82 |

|

Cull rate |

30% |

33% |

45% |

35% |

29% |

43% |

| Table 4.2. DBAP 2005 Summary - Revenues and expenses by assets per cow and liabilities per cow ($/cwt). | ||||||

|

|

Assets ($ / cow) |

Liabilities ($ / cow) |

||||

|

Category |

< $4,000 |

$4,000-$5,600 |

> $5,600 |

< $1,340 |

$1,340-$2,500 |

> $2,500 |

|

Number of farms |

7 |

7 |

7 |

7 |

7 |

7 |

|

Revenues: |

|

|

|

|

|

|

|

Milk sold |

18.53 | 18.31 | 17.88 | 18.26 | 18.55 | 17.92 |

|

Raised, leased cow sales |

0.51 | 0.78 | 1.39 | 0.79 | 0.05 | 1.84 |

|

Heifer sales |

0.35 | 0.55 | 0.45 | 0.49 | 0.58 | 0.29 |

|

Gain on purchased livestock sales |

(0.01) | (0.58) | 0.20 | 0.04 | (0.40) | (0.04) |

|

Other revenues |

0.80 | 1.30 | 1.73 | 1.03 | 1.02 | 1.78 |

|

Total revenues |

20.18 |

20.37 |

21.65 |

20.61 |

19.80 |

21.79 |

|

Expenses: |

|

|

|

|

|

|

|

Personnel |

2.86 | 3.14 | 4.51 | 4.31 | 2.85 | 2.35 |

|

Purchased feed |

7.64 | 7.88 | 6.14 | 6.95 | 6.90 | 7.81 |

|

Crops |

0.15 | 0.35 | 0.73 | 0.58 | 0.25 | 0.40 |

|

Machinery |

0.88 | 0.99 | 1.46 | 1.38 | 0.78 | 1.17 |

|

Livestock |

2.30 |

1.37 |

2.37 |

2.60 |

1.67 |

1.76 |

|

Milk marketing |

1.23 |

1.21 |

1.24 |

1.09 |

1.28 |

1.30 |

|

Buildings and land |

0.73 | 0.48 | 1.01 | 0.88 | 0.56 | 0.79 |

|

Interest |

0.51 | 0.59 | 0.90 | 0.13 | 0.62 | 1.24 |

|

Depreciation: |

||||||

|

Livestock |

1.03 | 1.36 | 0.94 | 0.20 | 1.36 | 1.77 |

|

Machinery |

0.60 | 0.54 | 1.30 | 0.97 | 0.66 | 0.81 |

|

Buildings |

0.21 |

0.33 |

0.62 |

0.31 |

0.25 |

0.61 |

|

Other expenses |

1.01 |

0.84 |

1.18 |

1.09 |

0.94 |

1.00 |

|

Total expenses |

19.14 | 19.08 | 22.39 | 20.48 | 18.13 | 22.00 |

|

Net farm income from operations |

1.04 | 1.29 | (0.73) | 0.13 | 1.67 | (0.21) |

|

Gain on sale of capital assets |

(0.01) | (0.15) | (1.22) | (0.78) | 0.13 | (0.74) |

|

Net Farm Income |

1.03 | 1.13 | (1.96) | (0.65) | .80 | (0.94) |

| Table 4.3. DBAP 2005 Summary - Financial performance by assets per cow and liabilities per cow. | ||||||

|

|

Assets ($ / cow)

|

Liabilities ($ / cow) |

||||

|

Category |

< $4,000 |

$4,000-$5,600 |

> $5,600 |

< $1,340 |

$1,340-$2,500 |

> $2,500 |

|

Number of farms |

7 |

7 |

7 |

7 |

7 |

7 |

|

Liquidity: |

|

|

|

|

|

|

|

Current ratio |

1.82 |

2.58 |

12.94 |

2.27 |

1.37 |

13.70 |

|

Working capital ($) |

234,881 |

240,634 |

(106,309) |

224,631 |

172,138 |

(27,563) |

|

Solvency: |

|

|

|

|

|

|

|

Debt to asset ratio |

0.50 |

0.43 |

0.25 |

0.14 |

0.53 |

0.51 |

|

Equity to asset ratio |

0.50 |

0.57 |

0.75 |

0.86 |

0.47 |

0.49 |

|

Debt to Equity Ratio1 |

6.02 |

0.92 |

0.47 |

0.19 |

4.11 |

3.11 |

|

Profitability: |

|

|

|

|

|

|

|

Rate of return on assets |

0.06 |

0.06 |

0.00 |

0.04 |

0.08 |

0.01 |

|

Rate of return on equity |

0.02 |

0.08 |

(0.03) |

0.05 |

0.18 |

(0.16) |

|

Operating Profit Margin Ratio |

0.05 |

0.07 |

(0.07) |

(0.02) |

0.09 |

(0.02) |

|

Financial efficiency: |

|

|

|

|

|

|

|

Asset turnover rate |

1.13 |

0.81 |

0.39 |

0.77 |

0.96 |

0.61 |

|

Operating expense ratio |

0.83 |

0.80 |

0.87 |

0.91 |

0.77 |

0.81 |

|

Depreciation expense ratio |

0.09 |

0.11 |

0.13 |

0.07 |

0.12 |

0.14 |

|

Interest expense ratio |

0.03 |

0.03 |

0.04 |

0.01 |

0.03 |

0.06 |

|

NFIFO Ratio2 |

0.05 |

0.06 |

(0.04) |

0.01 |

0.08 |

(0.01) |

|

Repayment capacity: |

|

|

|

|

|

|

|

Cash flow coverage ratio |

1.10 |

3.89 |

12.88 |

0.92 |

1.11 |

15.83 |

|

Term Debt Coverage Ratio3 |

1.57 |

6.04 |

1.08 |

1.80 |

6.08 |

0.81 |

|

Capital Replacement Margin4 ($) |

458,418 |

684,602 |

(178,473) |

499,638 |

349,460 |

115,449 |

2 Net farm income from operations ratio.

3 Term debt and capital lease coverage ratio.

4 Capital replacement and term debt repayment margin.

| Table 4.4. DBAP 2005 Summary - Balance sheet by assets per cow and liabilities per cow ($/cow). | ||||||

|

|

Assets ($ / cow) |

Liabilities ($ / cow) |

||||

|

Category |

< $4,000 |

$4,000-$5,600 |

> $5,600 |

< $1,340 |

$1,340-$2,500 |

> $2,500 |

|

Number of farms |

7 |

7 |

7 |

7 |

7 |

7 |

|

Balance Sheet (January 1): |

|

|

|

|

|

|

|

Current assets |

264 |

392 |

629 |

377 |

407 |

501 |

|

Total Assets |

3,194 |

4,380 |

12,825 |

9,048 |

3,622 |

7,730 |

|

Current liabilities |

539 |

629 |

354 |

350 |

505 |

667 |

|

Total Liabilities |

1,442 |

1,830 |

2,157 |

571 |

1,783 |

3,075 |

|

Equity |

1,752 |

2,550 |

10,668 |

8,477 |

1,838 |

4,655 |

|

Balance Sheet (December 31): |

|

|

|

|

|

|

|

Current assets |

349 |

544 |

566 |

338 |

643 |

478 |

|

Total Assets |

3,397 |

4,636 |

11,970 |

8,657 |

3,986 |

7,360 |

|

Current liabilities |

275 |

541 |

342 |

249 |

509 |

400 |

|

Total Liabilities |

1,614 |

1,972 |

2,103 |

621 |

1,921 |

3,147 |

|

Equity |

1,784 |

2,665 |

9,867 |

8,037 |

2,065 |

4,213 |

Figures

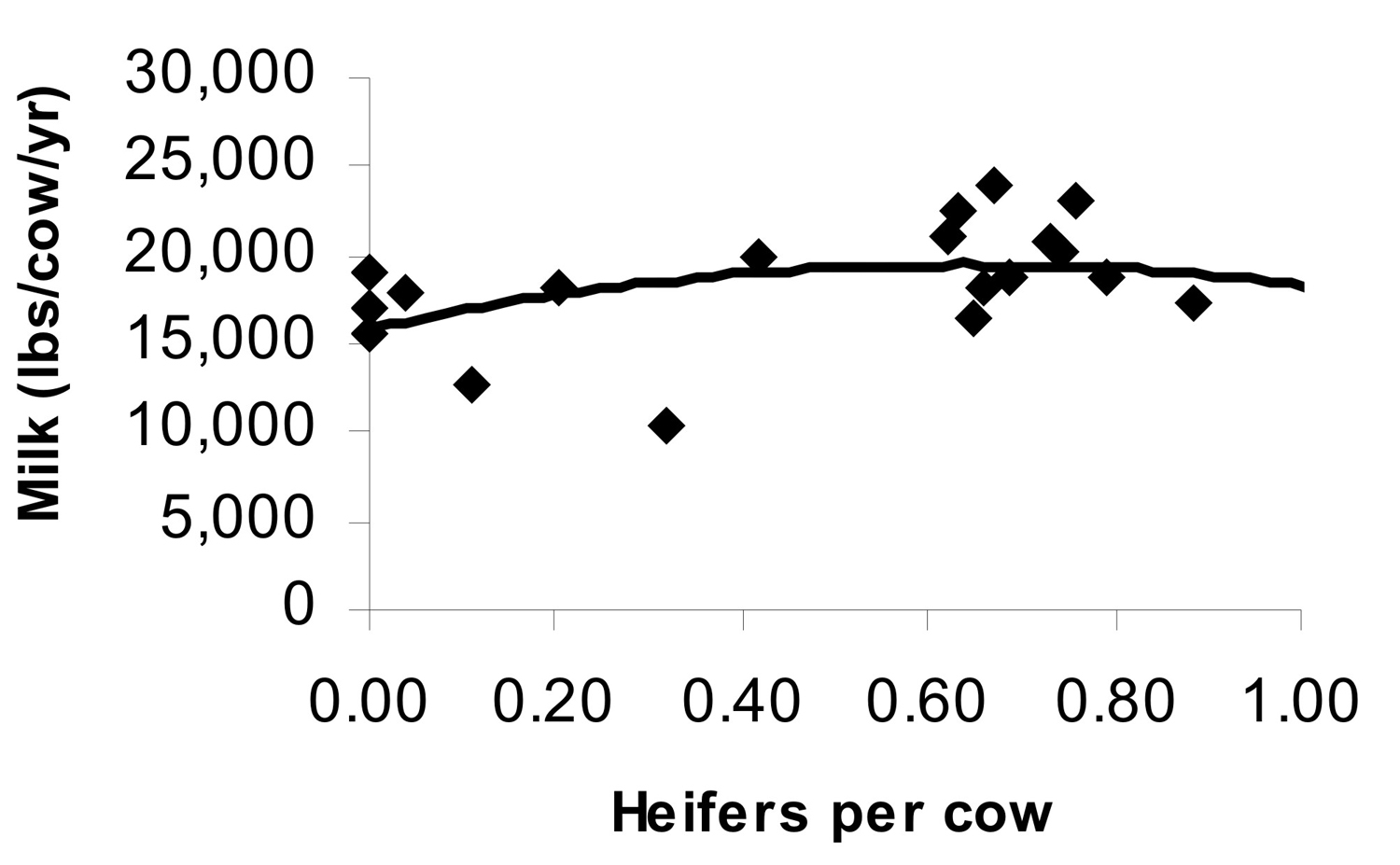

Figure 1. DBAP 2005 Summary – Milk production (lb / cow / year) by heifers per cow.

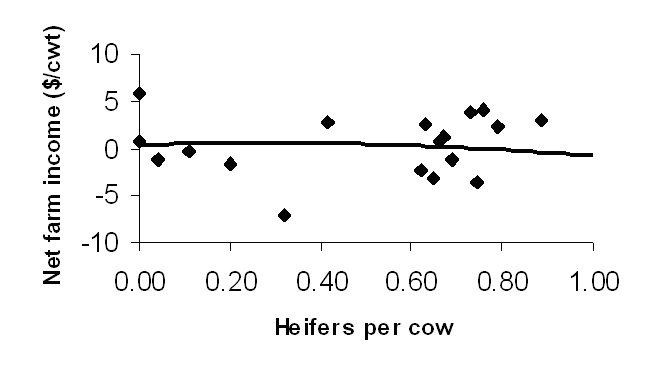

Figure 1. DBAP 2005 Summary – Milk production (lb / cow / year) by heifers per cow. Figure 2. DBAP 2005 Summary - Net farm income ($ / cwt.) by heifers per cow.

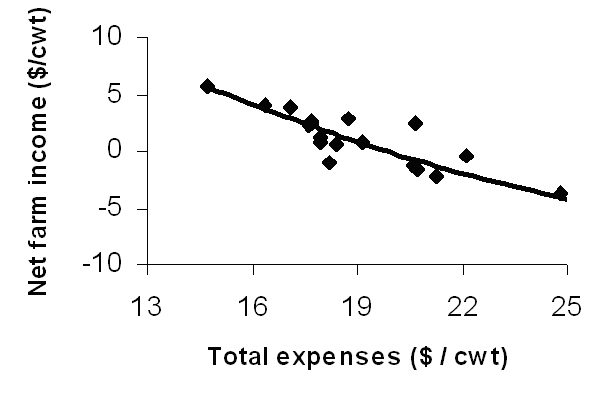

Figure 2. DBAP 2005 Summary - Net farm income ($ / cwt.) by heifers per cow. Figure 3. DBAP 2005 Summary - Net farm income ($ / cwt.) by total expenses ($ / cwt.).

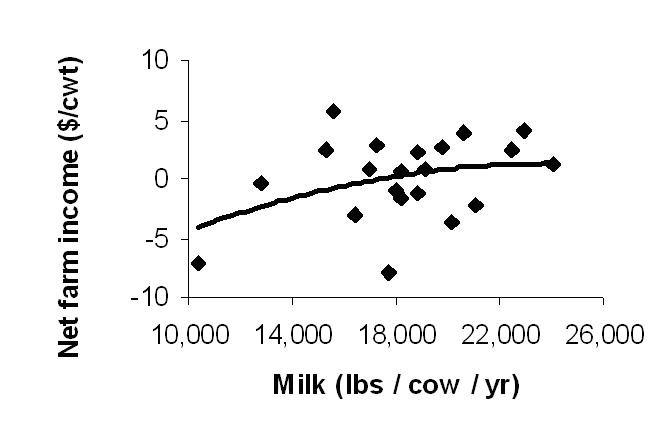

Figure 3. DBAP 2005 Summary - Net farm income ($ / cwt.) by total expenses ($ / cwt.). Figure 4. DBAP 2005 Summary - Net farm income ($ / cwt.) by milk yield (lbs / cow / year).

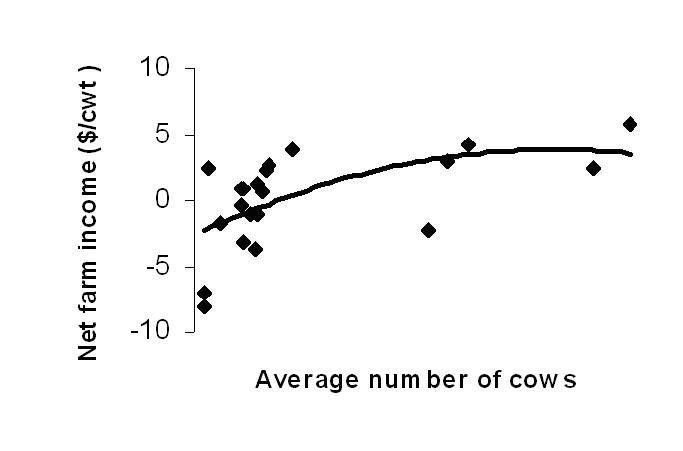

Figure 4. DBAP 2005 Summary - Net farm income ($ / cwt.) by milk yield (lbs / cow / year). Figure 5. DBAP 2005 Summary - Net farm income per cwt. ($) by average number of cows. The x-axis is not displayed to avoid possible identification of dairy farms.

Figure 5. DBAP 2005 Summary - Net farm income per cwt. ($) by average number of cows. The x-axis is not displayed to avoid possible identification of dairy farms.

1 L. Ely, Professor, Department of Animal and Dairy Science, University of Georgia, Athens, Georgia 30602;

2 R. Giesy, Extension Agent IV; B. Broaddus, Extension Agent I; C. Vann, Extension Agent II; A. Bell, Graduate Student;

A. De Vries, Assistant Professor, Department of Animal Sciences, Cooperative Extension Service,

Institute of Food and Agricultural Sciences, University of Florida, Gainesville, Florida 32611

Status and Revision History

Published on Jun 04, 2007

Published on Feb 04, 2009

Published on Jun 01, 2010

Published with Full Review on Jun 17, 2013